Beginning August 1, 2023, China has imposed export restrictions on gallium (Ga) and germanium (Ge) products.

These restrictions are seen as a retaliation against U.S. and EU sanctions on China, which have restricted the export of chips and chipmaking equipment. According to Wei Jianguo, former vice minister of commerce, China’s latest export curbs are just a starting point and China has other sanction options should the United States impose stricter technology restrictions on it.

In fact, China has been signaling that it may restrict the export of rare earth minerals to the United States as the trade conflict between the two countries escalates.

China’s controls will reportedly apply to eight Ga products: gallium antimonide, gallium arsenide (GaAs), gallium metal, gallium nitride (GaN), gallium oxide, gallium phosphide, gallium selenide and indium gallium arsenide.

They will also apply to six Ge products: germanium dioxide, germanium epitaxial growth substrate, germanium ingot, germanium metal, germanium tetrachloride, and zinc germanium phosphide.

Chinese exporters will be required to obtain licenses from the commerce ministry to continue shipping these materials out of the country. Additionally, they must provide comprehensive information about overseas buyers and their applications. As of now, there are no outright bans on specific countries or end users.

In the short term, these controls look likely to lead to higher prices for Ga and Ge, as well as longer delivery times.

However, the dependency of major Chinese smartphone manufacturers like Vivo, Oppo, Xiaomi, and Honor on foreign suppliers for GaAs-based components is a fascinating paradox. China lacks viable domestic suppliers for RF components and modules, specifically in the realm of GaAs-based technology. Thus, these Chinese companies rely heavily on overseas sources such as Broadcom, Skyworks, Qorvo, and Qualcomm to fulfill their demand for such components. It is thus expected that US and European companies, especially the ones involved in supplying RF components, will still be able to source Ga from China.

Background

In Jan 2021 the Dept of Energy released the report “Critical Minerals and Materials”, which listed the DOE’s strategy to support domestic critical mineral and materials supply chains.

In 2022, the United States Geological Survey released a new list of 50 mineral commodities critical to the U.S. economy and national security after an extensive multi-agency assessment. The Energy Act of 2020 defines a “critical mineral” as “a non-fuel mineral or mineral material essential to the economic or national security of the U.S. and which has a supply chain vulnerable to disruption”. Critical minerals are also characterized as “serving an essential function in the manufacturing of a product, the absence of which would have significant consequences for the economy or national security”. Ga and Ge are both on that list.

They are also both listed on the “35 Minerals Absolutely Critical to U.S. Security” list.`

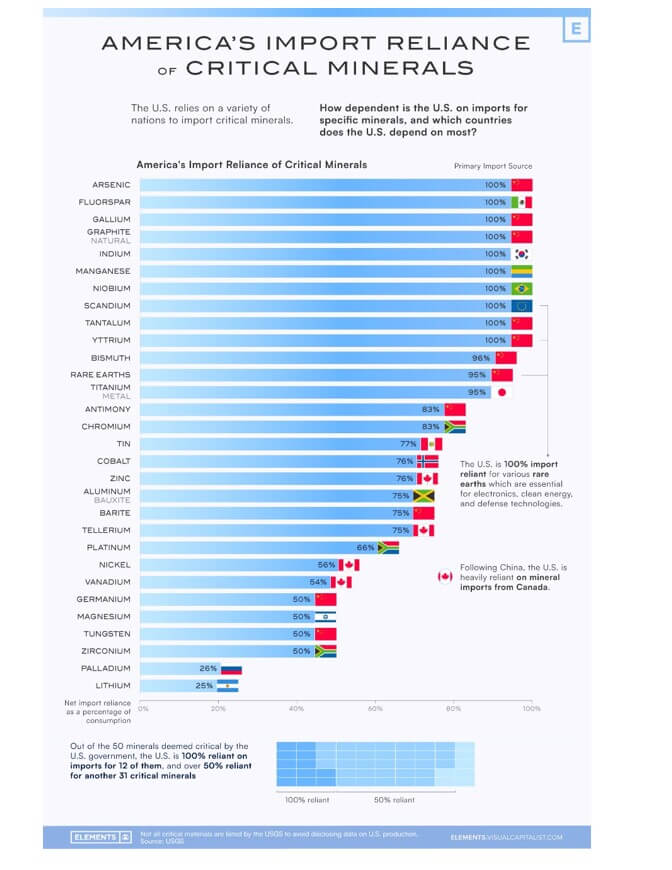

It can be seen in the chart below that we rely heavily on China for the purchase of many of these materials including Ga and Ge.

From these studies, it is obvious that China dominates either the mining process or the refining process of most critical minerals.

China’s Ga and Ge position

China dominates the world’s supply chain by being able to use cheap coal power, low wages and lax environmental regulations to perform the processing for the extraction of these minerals. China has exported Ga and Ge relatively cheaply, allowing China to become the dominant global supplier. Although the metals are not rare, they have been kept cheap by China and can be relatively expensive to mine elsewhere.

China produces approximately 60% of the world’s Ge and approximately 80% of its Ga, according to the Critical Raw Materials Alliance (CRMA), a European industry association.

China controls about 60% of all Ge supplies. The element is derived in two main ways, as a by-product of zinc production and from coal. These respectively account for about 75% and 25% of the total supply.

Other Sources of Ga and Ge

These elements are not rare, it’s the processing capacity that’s the issue. There is no reason that the US could not process these materials. The issue is cost. It costs more to process in the US than in China. Someone needs to make the investment and have the Government and industry support to build the plants required. The trouble is, they can do that, but if China then lifts the ban, the end users will go back to the cheapest source.

Most Ge is a by-product of zinc production and from coal fly ash. China produces around 60% of the world’s Ge, with the rest coming from Canada, Finland, Russia, and the United States. Gallium is found in trace amounts in zinc ores and in bauxite, and Ga metal is produced when processing bauxite to make aluminum. Approximately 80% is produced in China, according to the CRMA. China exported 43.7 metric tons of unwrought and wrought Ge and 94 metric tons of Ga in 2022.

Should disruptions occur, however, the metals and mining industry has options to help plug the shortfall. For example, in the United States and Australia, Ge and Ga can be recovered as by-products from zinc and alumina refineries. However, it will take time to put the infrastructure in place.

Ge and Ga Applications

Germanium is used in military applications such as night-vision devices, as well as satellite imagery sensors and SiGe for fiber optic communications. Ge-based solar cells power a significant number of satellites used in space missions. Ge is particularly useful in space technologies such as solar cells because it is more resistant to cosmic radiation than silicon.

95% of Ga is used to make GaAs for use in microelectronics. Only a few companies – one in Europe and the rest in Japan and China – can make it at the required purity, says the CRMA. The Canadian company, Neo Performance Materials, also claims to make Ga at the required purity. GaAs is used in radar and radio communication devices, consumer electronics, automotive, military, RF, and optical communications. satellites and LEDs.

Meanwhile, GaN is used in semiconductors in components for things like electric vehicles, sensors, high-end radio communications, LEDs, and Blu-Ray players. Its use is expected to grow significantly.

The export rules on Ga and Ge could lead to a potential disruption in the supply chain for these substrate manufacturers.

GaAs & Ge Substrate Production

Gallium raw materials comprise ~ 50% of the GaAs substrate price. This should produce uncertainty and potential price volatility in the GaAs and Ge substrate market.

On the other hand, the impact on GaN-on-Si and GaN-on-SiC wafers pricing, which are mainly used for power and RF applications, might not be as severe as the Ga-based and Ge substrates. This is because GaN epitaxy uses Ga sources in low quantities, to produce layers only a few micrometers in thickness.

Companies like AXT (US), Freiberger (Germany), and Sumitomo Electric (Japan) are GaAs substrate suppliers. AXT has a significant reliance on China. AXT manufactures all its products in China and partially owns Chinese raw material companies producing high-purity gallium. AXT’s Chinese subsidiary, Tongmei, is currently seeking permits to export GaAs and Ge substrates.

Defense Strategic Stockpiles

U.S. imports of gallium metal and GaAs wafers in 2022 were worth about $3 million and $200 million, respectively, according to USGS.

The Defense Department has a strategic U.S. stockpile for Ge, but currently has no inventory reserves for Ga.

Major defense contractors do not buy Ga and Ge directly but rather purchase semiconductors from suppliers who source Chinese Ga and Ge. Restrictions on that supply will potentially slow down the production of DOD systems and/or drive up their cost.

The DoD will eventually have to find alternate sources for gallium and germanium “whether it’s direct mining, direct manufacture, direct refining or production, or from a recycling program from obsolete equipment.”

For all the latest in Advanced Packaging stay linked to IFTLE……………….