THE CHIPS and Science Act passed to great industry enthusiasm last month. Françoise wrote about the CEO Summit and some of the CEO’s thoughts on that celebratory day. But as I poorly paraphrase Aart De Geus, “Today we celebrate the success of this event (CHIPS) as co-collaborators, tomorrow it’s back to work as competitors.”

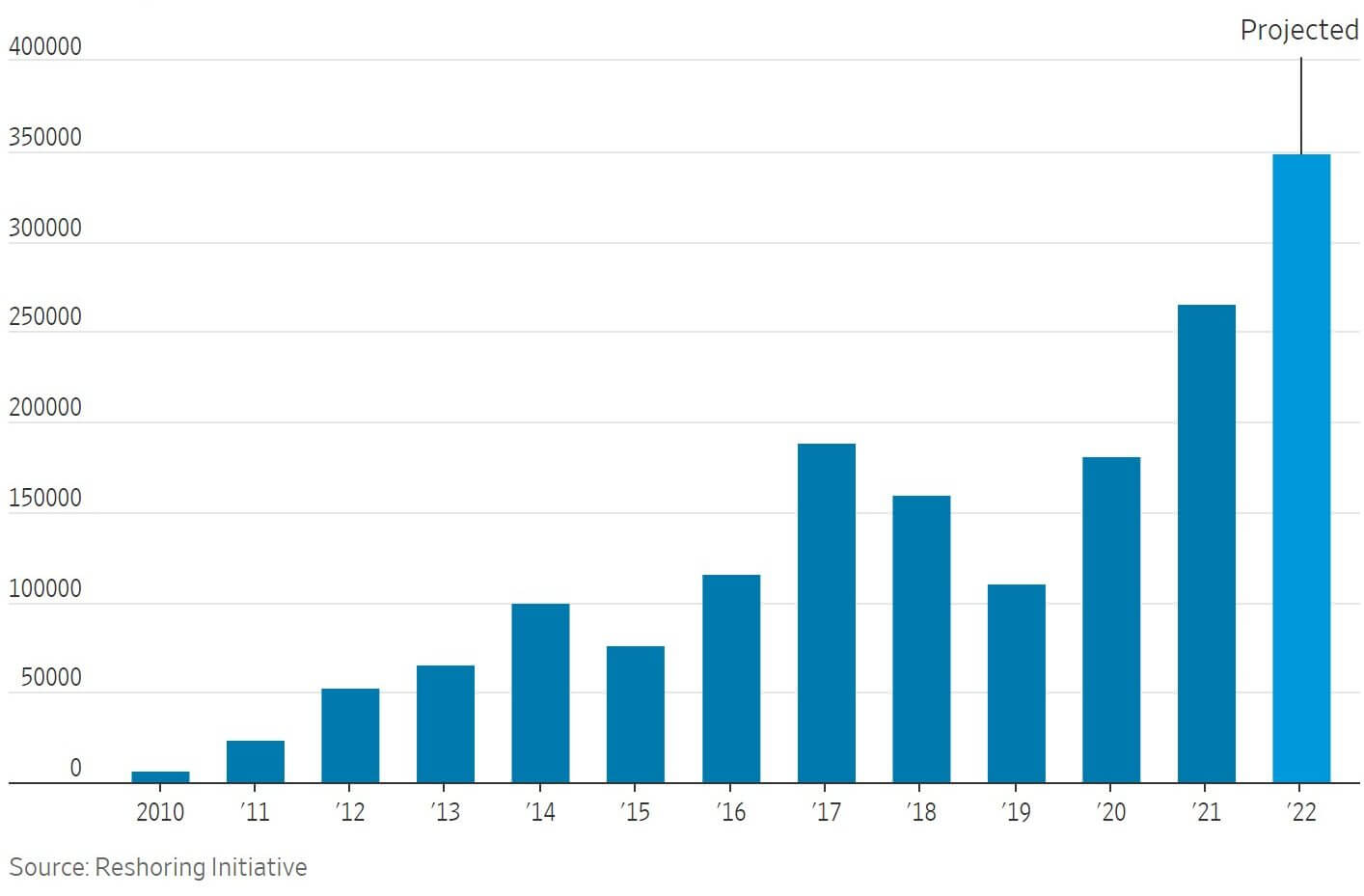

So, let’s take a look at what “back to work” looks like. According to the Wall Street Journal, companies have announced over 350,000 jobs that will be brought back to America as a result of reshoring. This may not all be due to the CHIPS and Science Act and the Inflation Reduction Act of 2022, but there have been a lot of announcements over the past year of new fabs coming back to the US.

This is not all Semiconductor manufacturing jobs, but a considerable amount of technology and construction jobs, as 7000 construction workers are needed for Intel’s site in Ohio. This will put a huge pinch on the already tight workforce for the chip industry.

Getting back to work means big investment and building a significant number of fabs in the US. Below is a listing of new fabs both in the US and Europe, most of which were announced with execution tied to government funding, or in the case of the JASM fab in Japan, a reshoring of technology.

Semiconductor Company Investments in the US and Europe because of the respective CHIPS legislation

- Intel: Ohio $20 billion, New Mexico, Arizona $20 billion, Germany $17 billion, Italy TBD $ 5 billion, Leplix $12 billion.

- GF: Malta, ST Microelectronics JV in Grenoble for SOI $ from France, Qualcomm long-term purchase agreement, Google, joins Open-Source Silicon Initiative.

- Global Wafers: Sherman Texas $3.4 billion

- Micron $40 billion.

- Sky Works: with Purdue University 1.8 billion.

- TSMC: Arizona, $12 billion, JV with Sony& Denso, Japan (JASM)

- Samsung: Taylor TX, $17 billion (another possible $192 billion, 11 fabs); $15 B investment in R&D Center Korea

- SK Hynix: Packaging facility in the U.S.

- SEH: 300,000 sq. ft. addition to Vancouver, Washington site.

- Bosch: 300 mm expansion, Europe

I would expect more to be coming, and with the inflation/energy legislation passed in late August, there are other factory announcements. In addition to the packaging facility, SK Hynix will also be building a battery factory and bioscience facility in the US. There may be more to come.

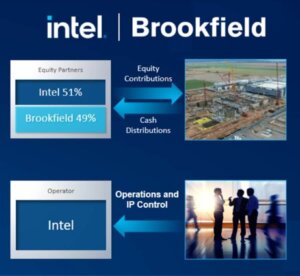

As you look at these announcements, from an investment standpoint it is massive. As I was putting together the numbers, I was thinking about how Intel was going to manage the capital outlay they have announced. Then Intel announced an equity partnership with Brookfield Asset Management, that will reduce Intel’s capital outlay by about half for what appears to be the Arizona fabs. The SEC filing states that Brookfield will provide 14.2 billion in cash to the partnership, and Intel provides $14.8 billion. It will be interesting to see how many of these investment partnerships emerge as the semiconductor industry expands on this massive scale. If the industry does grow to a trillion dollars before the end of the decade, this investment by Brookfield could prove to be very profitable.

At the moment, TSMC, Intel, and Samsung look to be positioned to spend as much as $300 billion In capital expenditures worldwide over the next 3 years. Add in investments by SK Hynix, Micron, and Kioxia, along with the other chip manufacturers and you have a very healthy fab construction and equipment industry both in the US as well as in each company’s home base.

With $39 billion for fab construction allocated in the CHIPS and Science Act, it is a small percentage of the capital spending that will take place over the next 10 years, perhaps more important to all of these companies is the tax incentives that will be very beneficial to the bottom line. Nevertheless, the result of the CHIPS and Science Act is a staggering amount of investment over a short period of time, and hopefully, the end markets will be able to absorb all of the chips that these fabs will produce.

Education

One of the challenges of this massive investment will be finding the engineers and technicians to support the multiple fabs being built. Part of the CHIPS and Science Act will provide $200 million to develop training programs.

Recently, it seems that companies want engineers trained prior to walking in the front door. In the dark ages of the industry, this was not possible as there were no semiconductor tracks at universities. Instead, companies hired chemical engineers, electrical engineers, chemists, and physicists and trained them to work in the fab. Texas Instruments had the nickname, “Training Institute”, as it had a great training program that in the long run, greatly benefited the rest of the industry.

At SEMICON West, Françoise interviewed Larry Smith, Chairman of TEL, General Paul Funk and Major Ray Wilson of the United States Army for the 3D inCites Podcast discussing the role veterans can play in the semiconductor industry. When I was active in the equipment industry, it was very common to have veterans in many different roles in the company. It’s good to see companies actively recruiting veterans for the semiconductor industry. This won’t fill all the openings, but it will put some great people in the industry.

While hiring veterans will be of significant benefit to the semiconductor industry, more interesting to me will be how the $200 million spreads out for training, and how to get individuals interested in semiconductor manufacturing. Shifting the needle from software to hardware could be challenging for the industry. There will also be the challenge of retention after training and living through the cycles of the industry. In the dark ages there were some brutal layoffs that sent engineers off to other careers. The industry will need to manage this carefully to have a successful reshoring effort. But for now, the capital expenditure gates have opened, so let’s get back to work and make the reshoring a success.