I spent last week attending two separate events: the opening of the Center for Heterogeneous Integration and Performance Scaling (CHIPS) at UCLA, and The MEMS Executive Congress, in Napa. I came away from both events with some interesting takeaways on new technology developments, which I plan to dive into and share in the coming week. But more importantly than that, I came away with some perceptions about the semiconductor and MEMS industries, and the ironic situation in which we now find ourselves. As we move towards the Internet of Things (IoT), the world will be more reliant on the technologies we manufacture, while at the same time, we are expected to offer these technologies at lower and lower prices, so that they are affordable to everyone. Yet there is one segment of the market that stands to profit enormously (and by profit I’m talking about revenues in the vicinity of $40B). The question is, how can the semiconductor and MEMS industry profit from the valuable data generated by their devices rather than finding ways to profit from chips and sensors that are becoming commoditized?

At the MEMS Executive Congress, Wouter Leibbrant, of NXP talked about how much it cost Bill Gates to make his home “smart” in 1995 ($1M), and how much computing power was involved (100 computers.) He compared that with today, where making a home smart runs about $1000; cheap enough so (almost) everyone can have one.

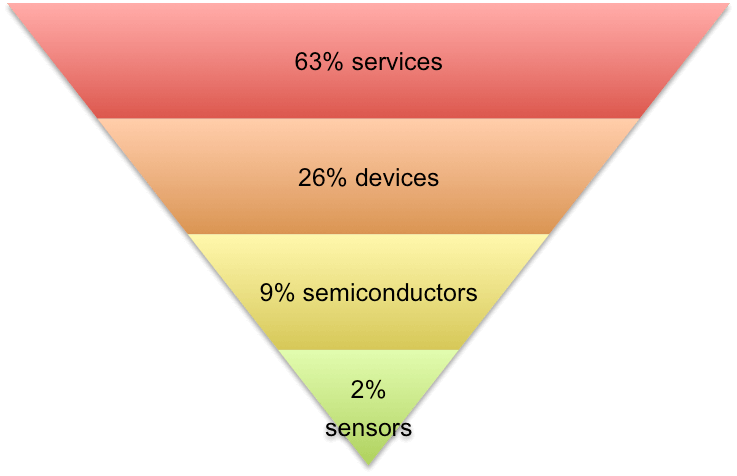

At CHIPS, Mark Ireland, VP of Market Development, Global Foundries, talked about how this is affecting the “disappearing middle class” in our industry, as mergers and acquisitions hit a record high of $120B in the first three months of 2015; more than double that of the previous five years combined. He also talked about our industry in transition thanks to pervasive computing and the IoT. As a result of the IoT, he said the value chain is shifting (figure 1).

These realities are driving semiconductor, MEMS and sensor manufacturers to try to figure out how to either reduce the costs of the technologies required to manufacture these necessary devices, or how to add value to them so that they can attach a higher ASP. I know this, because after all the speakers presented similar sobering information, they follow on with how their company, research institute, or university is finding ways to innovate, with the goal being either to reduce cost or add value.

Subu Iyer, director of CHIPS, explained their goal is to develop and “app-like” environment for hardware that can cut the time to market by 5-10X, and cut NRE cost by 10-20X, while allowing extreme heterogeneity including extensions to cyber-physical systems. In other words, they are find ways to deliver chips that do more, in less time, for less cost.

During MEMS Executive Congress, Steve Nasiri, Founder of InvenSense, an enormously successful fabless MEMS company, offered insight on how to model a fabless MEMS company after a fabless SEMI company to improve new designs’ time-to-market, manufacturing costs, and yields. Alissa Fitzgerald, AM Fitzgerald and Associates, talked about innovations under development, one of which is the concept of using paper as a substrate for sensors rather than silicon, because it offers a potentially lower sensor manufacturing cost, at higher throughputs and yields.

It was during two keynotes delivered by data analytics experts that the lightbulb went off in my head. Josh Knauer, president and CEO, Rhiza Labs, a market analytics firm, and John Thompson, general manager of advanced analytics for Dell Software, both highlighted how machine and sensor generated data adds value to critical processes within a variety of organizations, from surgical theatres in critical care hospitals, to retail establishments.

Thompson focused on using predictive models to convert raw data to smart data. One success story focused on using predictive models based on data collected in a surgical theater to reduce surgical site infection by 74%.

Knauer explained how his company’s goal is to assist its retail clients in making market-spend decisions to reach the right customers with the right data at the right time by providing observable data, rather than survey-based, self-reported data.

All market-spend decisions are based on five factors to understand consumer behavior: age, gender, income, education, and residence. Traditionally, that information came from survey-based, self-reported data. According to Knauer, what brands really need is observable data. For example, retailers want to know where someone is looking in a supermarket first, second, and third, combined with what’s in the shopping cart. MEMS and sensor technology, such as eye-tracking and image sensors, makes this possible.

Knauer said that annual market-spend for this type of research alone is $40B; and that’s the segment he could disrupt with access to the right information. He closed his speech with an appeal to the MEMS industry to help make this possible. After hearing that the MEMS industry stands to get 2% of this revenue according to the new value chain, it was all I could do to not stand up and say, “Oh really? How much is it worth to you.”

While it’s been abundantly clear that Big Data, and not the semiconductor and MEMS markets, will be the IoT winner when it comes to revenue, what we seem to forget, but what these two keynote speakers reminded us about, is that it all begins here. The semiconductor and MEMS industry provides the underpinnings of the IoT.

So not to over-simplify, but is it possible we are going about this all wrong? Maybe rather than a revenue model based on what consumers will pay for a particular device, we should by looking at what Big Data will kick in to get these technologies into the market space. I don’t have the answer to how that would work (if I did, I wouldn’t be writing this blog.) But it all starts with a shift in our own perception. They can’t do it without us. ~ F.v.T.

Interesting insight. Perhaps it is time for big data to kick in.

We are living in the age of information…