Day 2 of SEMI’s Innovation for a Transforming World featured the outlook on semiconductor market growth over the next 2-3 years. The pandemic to a certain extent has turned the semiconductor and the supporting markets on their head so to speak. After a strong 2018, 2019 saw slower growth. As slowdowns in the equipment space typically run 2-ish years, with the pandemic in March of 2020, I fully expected 2020 to see significantly slower growth, so did most of the forecasters when they published their Q1 and Q2 results.

By September the forecasters and industry were singing a different tune. Work from home and school from home had created a quick semiconductor turnaround and the semiconductor equipment market surged to 19% in 2019. 2021 is being driven by pandemic created semiconductor shortages and the growth of 5G, digitization of business (IoT), AI, renewable energy, electronics in vehicles, and current predictions are for strong semiconductor revenue growth and strong equipment growth.

Equipment and Materials Outlook

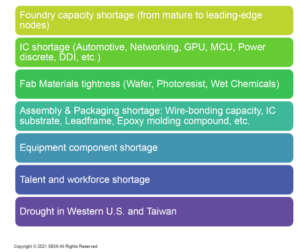

Clark Tseng started off Day 2 with the equipment and materials outlook. The worldwide GDP is booming and expected to grow at 5.4% year over year in 2021. This strong growth is one of the key drivers of semiconductor and semiconductor equipment revenue as the worldwide economy rebounds. Tseng pointed out that their area supply chain shortages across the board impacting the industry (Figure 1). The shutting of factories or slowing of the factories during the pandemic are impacting silicon and material supplies,

which in turn is exacerbating the chip shortages. No estimates were given on when a return to normalcy might occur, but estimates range from the end of 2021-2023 depending upon the sector.

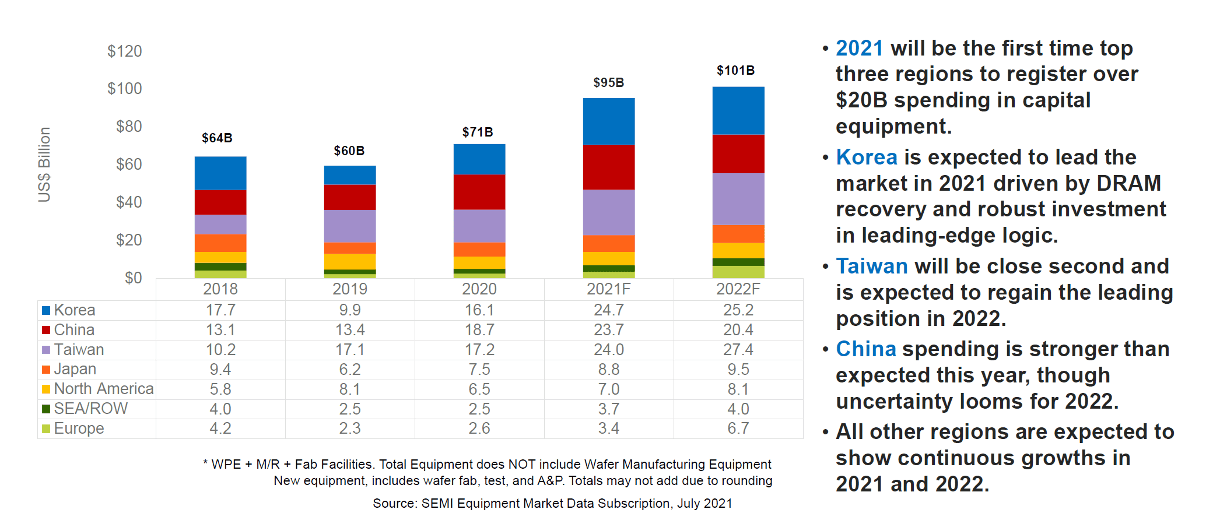

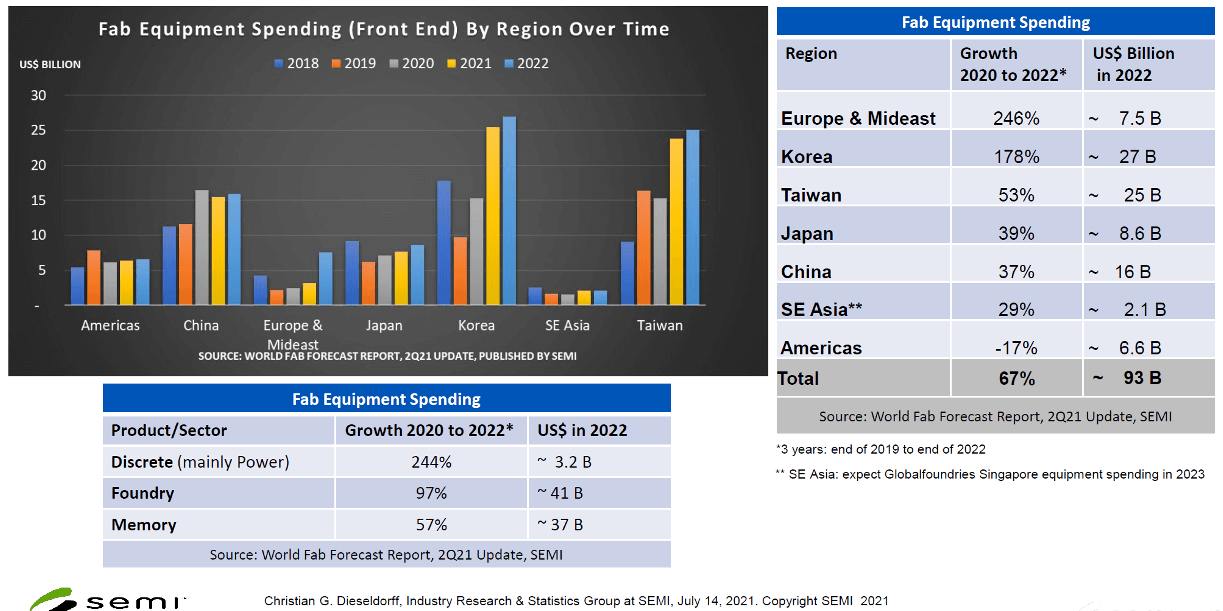

Capital spending is significant across all chip segments, and all regions (Figure 2). All regions are expected to show positive growth rates with Korea, Taiwan, and China all spending over $20 billion in capital expenditures for 2021

With the strong worldwide GDP driving demand and shortages of chips, there are limited headwinds to slow 2021 or 2022 estimates. There is the possibility of too much double ordering, which would result in canceled orders when supply and demand get back in balance. But at the moment the forecasted growth is positive and strong through 2022.

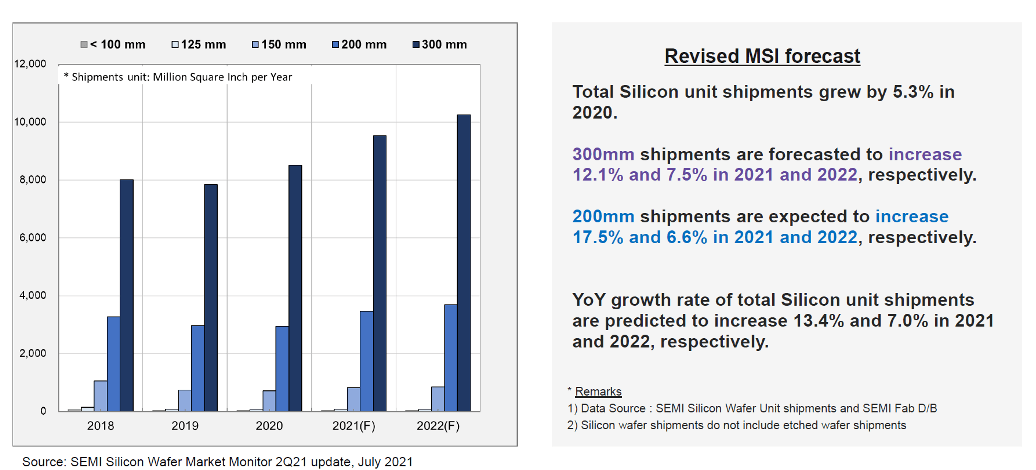

Tseng pointed out that silicon shipments are expected to grow to keep pace with the demand for chips (Figure 3). Global Wafers and GlobalFoundries recently signed an agreement where Global Wafers would increase 8-inch capacity to meet GlobalFoundries requirements. The growth of 8-inch silicon supplies is crucial to meet the demand of some of the key chip shortages and the new 8-inch fabs coming online.

One of the challenges for wafer expansion is that while there was tremendous growth—5% in 2020, and 13% year over year in June of 2021—the average selling price of silicon wafers in 2020 declined by nearly five cents per MSI. Lower profitability can limit the amount of cash flow needed for silicon manufactures to expand to meet demand. The merger of Global Wafers and Siltronic might help the supply-demand picture as Global Wafers has been expanding aggressively over the past several years, and if the merger goes through, they will be the second-largest silicon wafer manufacturer worldwide.

Global Fab Expansion

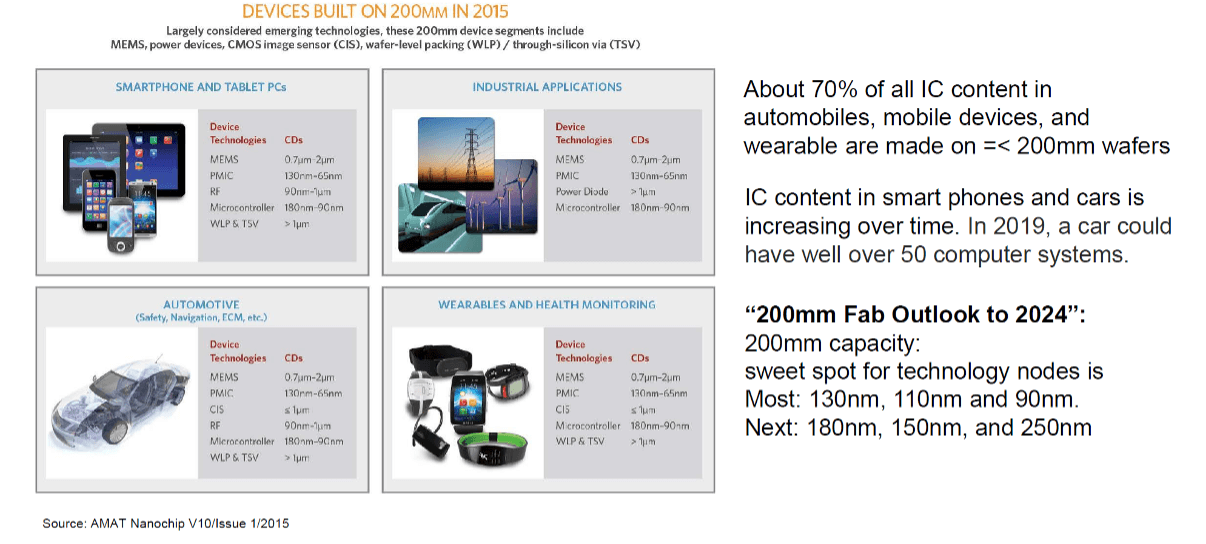

Transitioning from equipment and materials to the new fabs being built, Christian Dieseldorff of SEMI presented third in the day, following up on what Clark Tseng had discussed earlier. Much of the focus was on chip shortages and the reasons for them. Figure 4 demonstrates in part some of the reasons for shortages. Dieseldorff pointed out that over 70% of automotive chips are made on 200mm wafers, which for the most part are running at full capacity, so it will take time to catch up especially with the shutdowns that took place when orders for those chips seemed to be ramping.

The investment in new equipment and fabs to meeting demand is astounding. When you see Europe leading the pack in growth rates for fab equipment spending you know a significant investment is taking place worldwide. The fab equipment market is expected to reach $93 billion in 2022 (Figure 5). Marco Chisari of Bank of America titled his talk a New Golden Era. Being the skeptic I am paid to be, I’m wondering how long the Gold Rush lasts, or with all the new capacity being added there is the potential for a significant oversupply in the 2023–2025-time frame when all of these fabs come online and are looking for customers.

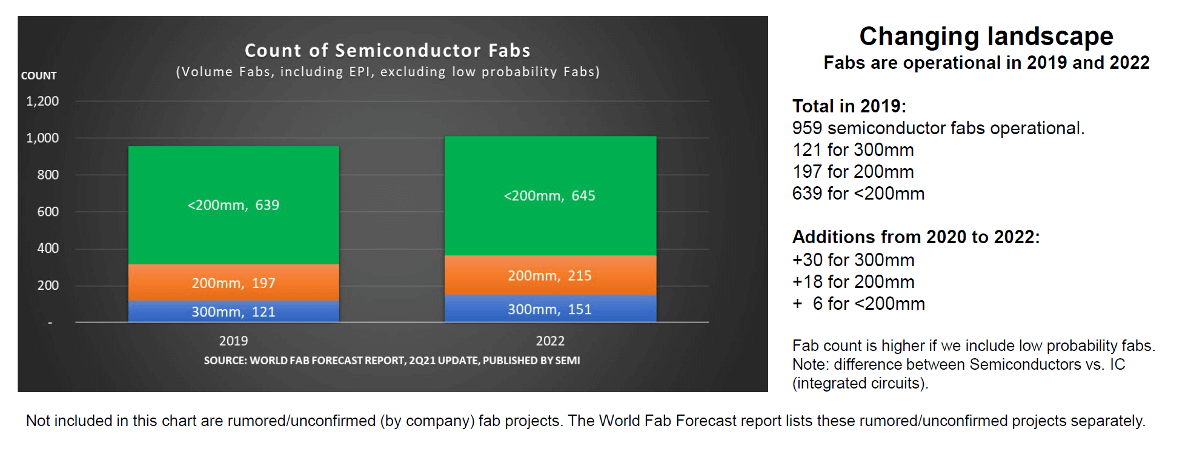

Dieseldorff presented on the new fabs coming online: >30, 300mm, 18, 200mm, and 6 or so at less than 200mm. the 6 below 200mm are for LED, or companies looking at SiC and GaN for power devices and do not impact the silicon side of the market. There is also the possibility of additional fabs if you look at the fine print at the bottom of the slide. Between 2020 and 2022 the industry is adding: 300mm ~2.9 million wafers per month; 200mm~ <= 980k wafers per month; for a 17% increase in wafer capacity (Figure 6).

A New Golden Era

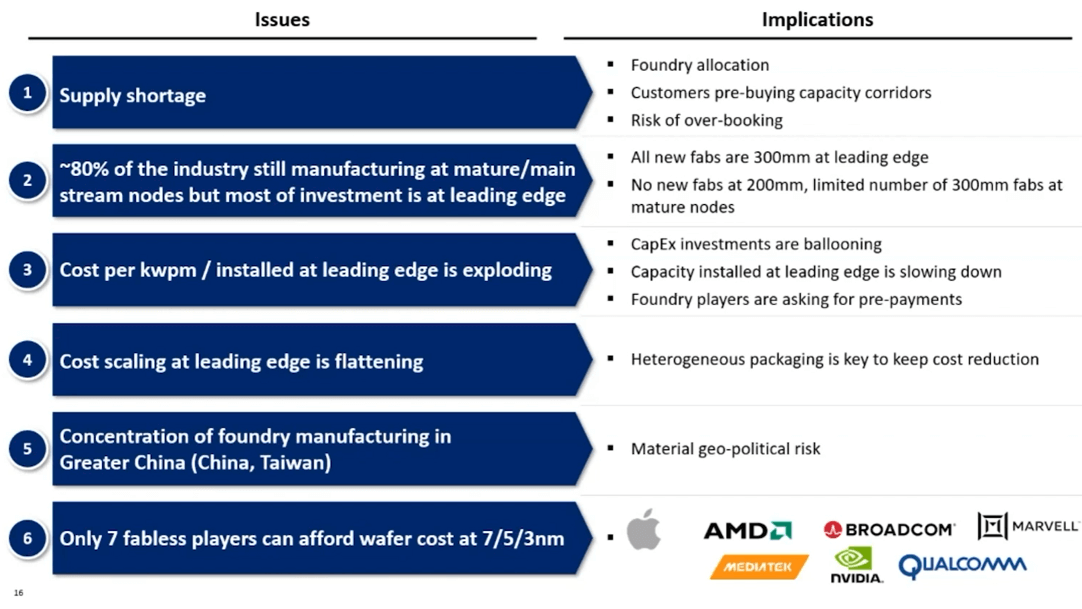

SEMI invited Marco Chisari of Bank of America to give his outlook on the forecast. He titled his talk, A New Golden Era and looked at the semiconductor industry from the stock market perspective. The industry has been on a strong growth curve growing semiconductor revenue from just over $100 billion in 2000 to a forecasted $ 625 billion in 2025. Chisari shared six major challenges he sees that are facing the semiconductor players. These are challenges that the industry struggles with on a daily basis as it charges forward (Figure 7).

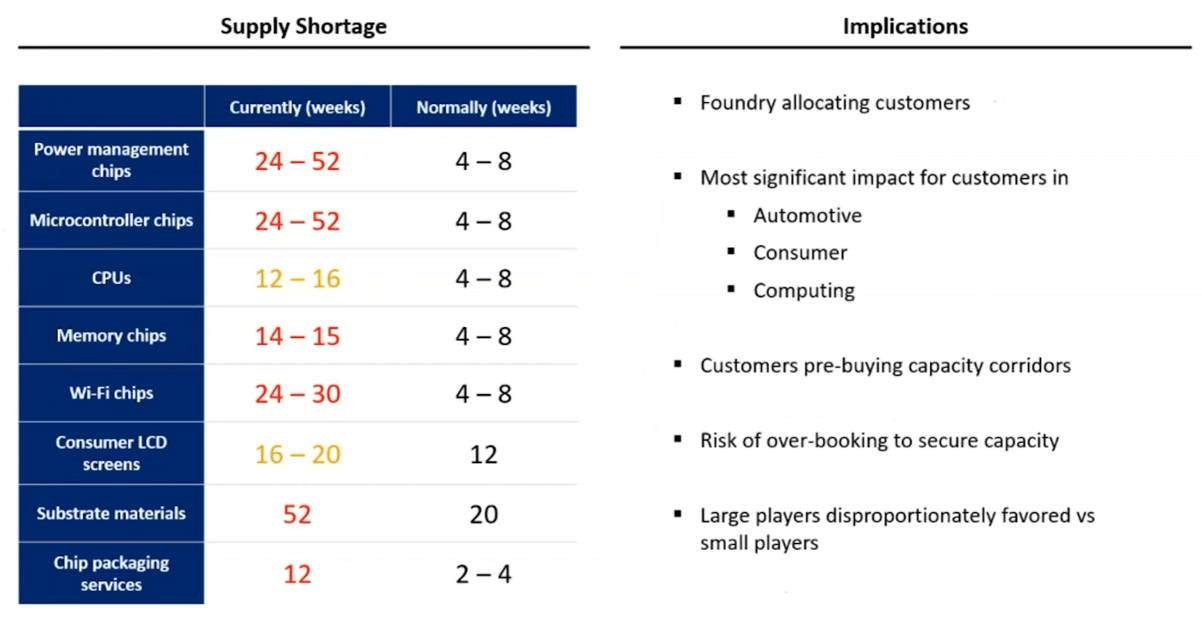

Chisari also shared Wall Street’s thoughts on chip shortages by looking at lead times for different chips, and their implications (Figure 8).

From my perspective, I think the key implication is that you have a lot of customers in line purchasing chips. In past cycles, this typically meant double ordering and ordering chips from multiple suppliers. One of the side impacts of the shortages is that the smaller foundries are seeing new orders, and are running closer to full capacity than they have historically. Chisari closed showing that the industry is in full rebound and that it is trending at an all-time high from a stock market perspective.

My takeaways from the forecasting portion of the conference are that the industry is booming and should continue to do so through 2022. Challenges will be getting the equipment and personnel needed to support the new fabs. Shortages will dissipate with time, and hopefully, double ordering, while the automotive industry and others restock will be kept to a minimum. If the stars stay aligned and there are no major economic hiccups hopefully that Golden Era will last for a while and the industry will enjoy a supercycle vesus a short-term cycle.