At the end of the 1st quarter and into early June, the thinking was that the semiconductor and packaging industry would have a rough 2020, or at least back-to-back down years. The impact of Covid-19, supply chain interruptions, and uncertainty surrounding Huawei all were creating fear, uncertainty, and doubt about how the industry would respond and what would be the financial impact on the industry.

In the first quarter, earnings reports at semiconductor manufacturers, OSATs and semiconductor equipment companies were significantly hedging their bets. Most did not give Q2 guidance and many painted a potentially bleak picture for the remainder of 2020, or at least until they gained a bit more visibility into the impact of the pandemic, and if their supply chains could recover.

Compounding the problem was the US commerce department’s actions against Huawei, which was a significant customer of TSMC and many worldwide semiconductor companies. TSMC, which typically has a good handle on business due to their visibility from incoming orders, was projecting a flat year for their 2020 business at the end of Q1, and on the whole, most forecasters updated their forecasts in April and May to reflect a flat to a negative outlook for the remainder of 2020.

Turn the page one quarter and it appears that the industry is humming along nicely, potentially much better than anyone expected. TSMC, while not fully committing to a number, believes that its growth in 2020 will be above 20%, a significant change in thinking from the previous quarter’s forecast.

If TSMC’s August revenue numbers are any reflection of the rebound, the industry is in for a positive year. TSMC’s August numbers hit records for revenue and were up 15.8% year over year. Intel, Samsung, Hynix, SMIC, and Micron, at the moment, are all looking at year over year growth. Intel is projecting 3% growth while Samsung is up 35% year over year for the first half of the year. So, for most of the top-tier chip companies, it appears to be a year of positive growth. According to the most recent World Semiconductor Trade Statistics (WSTS) release, they are forecasting the semiconductor industry to be up 3.3% for 2020. They state “This reflects an expected increase in Integrated Circuits, except Analog, with an increase from Memory at 15.0 percent, followed by Logic with 2.9 percent. In 2020, the Americas and the Asia Pacific are expected to grow.”

Company Financial Reports Quarter by Quarter

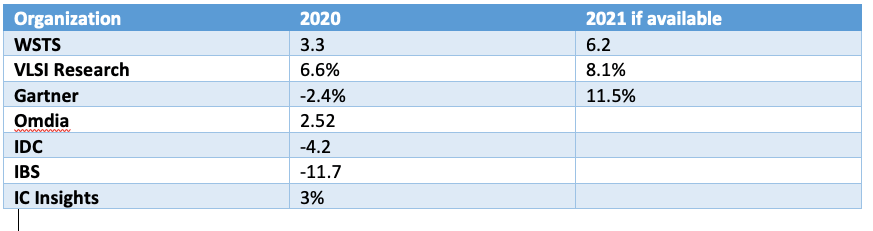

Below is a chart of the most recent forecasts by organizations such as WSTS, and industry analysts. It looks like the consensus is migrating towards three-percent growth. Most forecasting companies will update in late September, so it will be interesting to see where the consensus shifts to later in the month. Although, based upon the changes that are beginning to emerge, I would expect to see most forecasts turn positive unless they have strong convictions that significant weakness is expected in the fourth quarter.

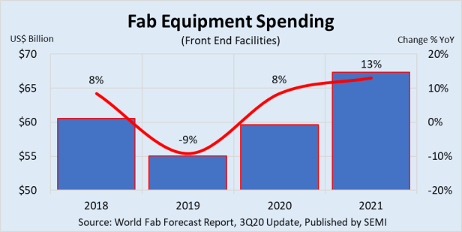

Equipment Spending Increasing

For fab equipment, SEMI just increased its forecast to 8% from 3% earlier in the year. TSMC increased Capex by $1 billion in its last earnings call to support 5nm and 3nm growth. Memories strong growth is driving new equipment purchases; however, the potential for the United States commerce department to stop US equipment manufactures selling to SMIC has the potential to lower the 2020 equipment spending by approximately $3 billion, as SMIC had raised their CAPEX to $6 billion for 2020 and had spent a bit over 2 billion at the end of the second quarter.

In the packaging sector, ASE revenues are up 18% year over year for the first half and Amkor’s Q2 revenue was up 31% year over year. Both companies have guided to potentially a flat Q3 based upon the licensing situation in China, and the uncertainty surrounding sales into that region. Communications were the key driver of revenues for both companies. Compute only accounts for approximately 15% of the two companies’ revenues so it the OSATs financials are not as good an indicator for the computing sector as TSMC or Intel numbers. Advanced packaging is a strong driver for both companies in 2020 as 5G begins to ramp and SIP applications continue to grow.

Industry Drivers

Work and school from home have been a big driver of computing technology in 2020 but reviewing the quarterly reports from TSMC, ASE, and Amkor, communications are playing a big role in the growth as 5G begins to emerge. TSMC’s revenues in the second quarter were driven primarily by the smartphone at 47% and then high-performance compute at 33% of the revenue respectively. 7nm accounted for 36% of TSMC’s revenue in the quarter. ASE and Amkor are seeing significant influence from 5G launches in the advanced packaging space. Communications and consumer applications are the two key drivers for ASE and Amkor in the OSATs space, with 5G just emerging.

The move to the cloud, IoT, and AI development are also growth factors in the semiconductor and packaging space with data center revenue at Intel accounting for 14.3 billion of Intel’s total revenue 39.5 billion in the first half of the year. Industrial and automotive markets took a short hiatus in Q2, but are expected to resume growth as IoT applications and as automation and EV moves forward in the automotive space.

Both personal computers and mobile devices are expected to slow in the remainder of 2020 and into 2021 as work from home purchases slow and the industry transitions to 5G.

The US and worldwide economies have rebounded faster than anticipated, but slowing is expected according to an economist survey in the Wall Street Journal. The WSJ reported on a worldwide basis the economy saw a rebound in the third quarter after a negative second quarter. The worldwide GDP, according to the International Monetary Fund (IMF) in June, is expected to be down 4.9% for 2020 growing to 5.4% in 2021. Economists expect the US unemployment rate to be 9% at the end of the year, Growth in the third quarter is expected to be 7%, after a contraction of 9% in the second quarter. Growth in the fourth quarter is expected to rise at 1.25% and is expected to reach pre-pandemic levels in 2022.

In looking to the 2021 forecast, I would expect the slowing of the GDP to potentially temper some of the strong semiconductor growth projected for 2021, but its very possible due to the slower 2020 for industrial growth, industrial could be a key driver in 2021 for the semiconductor space. How the economy and different countries recover will be one of the key assumptions for the 2021 forecast.

In Summary, 2020 for semiconductor and packaging is turning out much better than expected a quarter ago, and growth, while moderate growth is expected for 2021. Good news for the industry after a trying second quarter. ~ Dean