TSMC and the CHIPS & Science Act

I think it would be fair to say that most of us thought that TSMC would be getting their share of the CHIPS Act monies (Creating Helpful Incentives to Produce Semiconductors) to offset the costs of building its US fab/fabs in Arizona.

However, at a Taiwan Semiconductor Industry Association meeting on March 30, TSMC chairman Mark Liu was quoted as saying that “…certain supplementary restrictions and regulations in the United States’ CHIPS and Science Act are “unacceptable” and could dissuade potential partners from applying for the grant.”

Evidently, to receive money from the CHIPS Act fund, chipmakers must agree not to expand capacity in “foreign countries of concern,” such as China, for a decade and cannot engage in any joint research or licensing efforts with these countries involving sensitive technologies, according to rules by the U.S. Department of Commerce. Liu explained that further negotiations will have to be held with the U.S. so that the operations of Taiwanese companies like TSMC will not be adversely affected, but will instead enjoy a partnership that benefits Taiwan and the U.S.

SemiAnalysis on Recent TSMC Earnings

Dylan Patel and Gerald Wong at SemiAnalysis recently reported their thoughts on TSMC earnings. Since TSMC has such a large impact on the overall industry, let’s take a closer look.

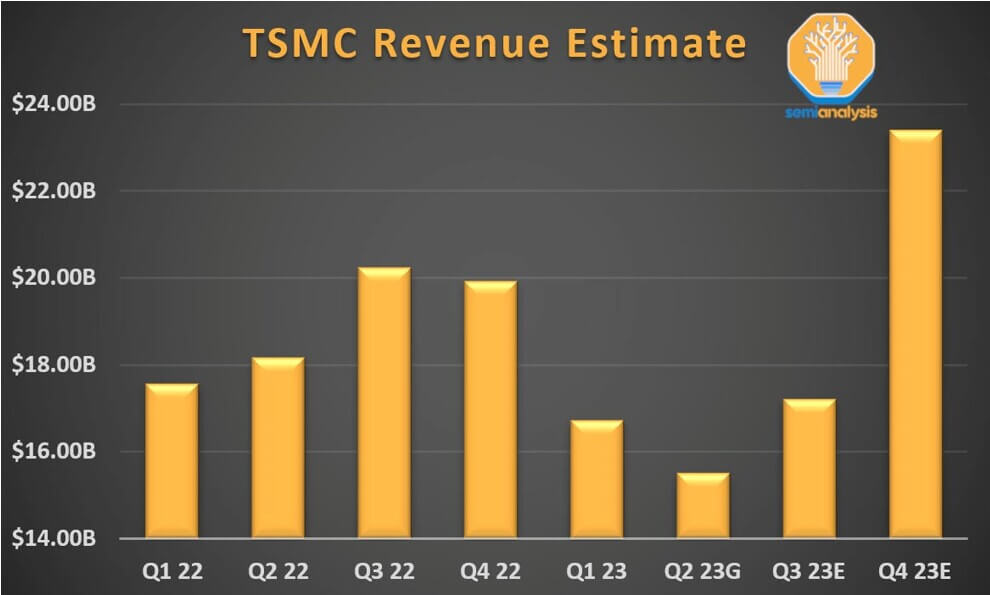

Revenue

TSMC revenue was down to $16.72B for Q1 2023, down 4.8% year on year. TSMC’s Q2 guidance implies earnings will fall to $15.6B by end of Q2, a 14.6% decrease year on year.

High-performance computing (HPC) is expected to grow from 42% to 44% of the company’s revenue. This segment includes both data center chips and laptop chips such as Apple’s M1. Despite growing as a percentage of revenue, the segment shrank by $1B or 27% quarter-on-quarter.

The smartphone picture looked the worst, with sales declining $1.8B for the quarter and also declining for the year. IoT continued to be strong with year-on-year growth despite quarterly weakness. While automotive grew ~50% year-on-year, it is showing signs of softening into second half of 2023.

Fab Utilization Rates

TSMC has enjoyed 100% utilization rates since the COVID boom started. The company had a big revenue and gross margin hit primarily due to its low utilization rates this quarter. TSMC’s 7nm node is the worst affected as far as utilization rates go, 4th Q ‘22 running at ~83% and in Q1 of ‘23 falling to below 70%. Reportedly Q2 ’23 will worsen (7nm utilization rates falling to below 60%) primarily due to weakness in both smartphones and PC sales.

Utilization rates for TSMC’s 5nm node is about 88%. It is far ahead of Samsung and Intel even three years after its initial shipments,. TSMC’s older nodes remained strong, although there were some signs of weakening, and they begin to free up capacity in Q2.

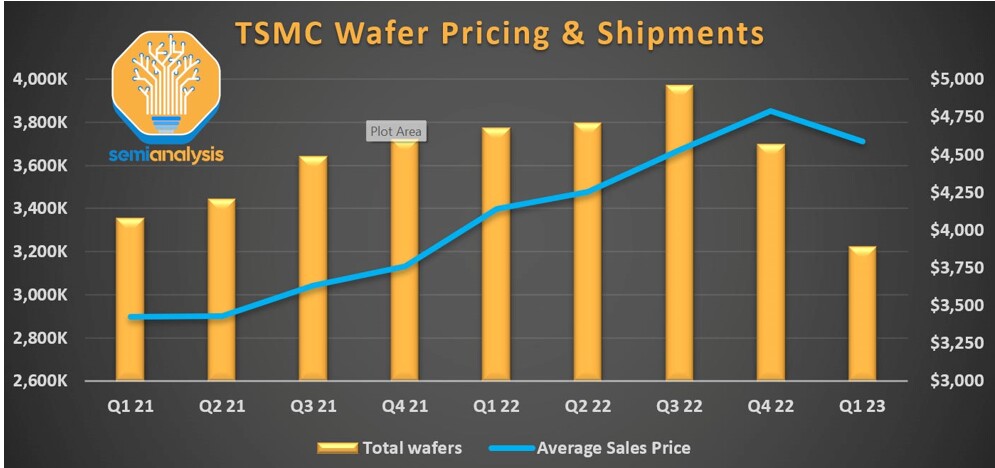

Pricing Declines

TSMC’s pricing (ASP) has also begun declining as is shown in Figure 2.

This pricing decrease is mostly a result of poor utilization of TSMC’s N7 process node.

3nm & 2nm Update

TSMC is seeing strong engagement on 3nm, with more than double the chip design tape-outs vs 5nm in the first two years of introduction. SemiAnalysis reports that this is due to the “tightening gap between smartphone and HPC product ramps”. Historically, smartphones have been the first to use new nodes, but with the advance of chiplets many HPC customers are reportedly wanting to get products on 3nm ASAP. 2nm is still expected to enter volume production in 2025.

Overseas Fabs

The US fab in Arizona is still expected to produce chips on the N4 process in late 2024. TSMC has reportedly hired more than 900 US staff for its Arizona fab. While costs will be higher than in Taiwan, TSMC believes customers will be willing to pay more per wafer if it comes from the US fab. Margins are expected to be in line with the company average.

TSMC’s 28nm Japan fab is also expected to commence volume production by late 2024. They are also expanding their 28nm fab in Nanjing, China to support their customers there. TSMC is also assessing the feasibility of a 28nm fab in Europe for automotive customers.

Advanced Packaging

TSMC indicated that advanced packaging revenue will decline due to customer demand, from 7% of total revenue in 2022 to 6-7% for 2023. This is driven by FOWLP, and weakness in mobile phone (Apple, MediaTek) sales.

TSMC is reporting a request for a large increase in CoWoS capacity. SemiAnalysis notes that the demands of AI training on memory performance are pushing designs to use High Bandwidth Memory (HBM), which requires advanced packaging technologies such as CoWoS. Nvidia is the largest customer of CoWoS ( A100 and H100 class data center AI GPUs) with Google (through Broadcom) the 2nd largest customer ( TPUv4 and TPUv5). Amazon’s Trainium through AI chip, as well as Microsoft’s new AI chips, also use CoWoS. Any one of these companies and, more likely all of them, are increasing spending heavily and require more CoWoS capacity.

IFTLE adds: Well so much for those prognosticators who declared that silicon interposers would never become a commercial success.

For all the latest on Advanced packaging stay linked to Insights from the Leading Edge (IFTLE) ……………

Feature photo credit: ChipsEtc.com – see more photos from their visit to Fab 21 here.