In Part 1 of my ISS 2020 blog, I described Monday’s opening keynote by LAM’s CTO, Richard Gottscho. He explained how valuable Coventor software is for minimizing trial and error loops in manufacturing. Part 1 also addressed Wall Street’s and market researcher’s thinking about the data explosion, our industry’s future, and summarized several presentations about innovative ways to utilize the power of semiconductors. Part 2 highlights sessions on technology, mobility, 5G, Asia markets, the future of Moore’s Law, and an investor’s panel. I conclude with some personal comments.

ISS 2020 Technology Updates

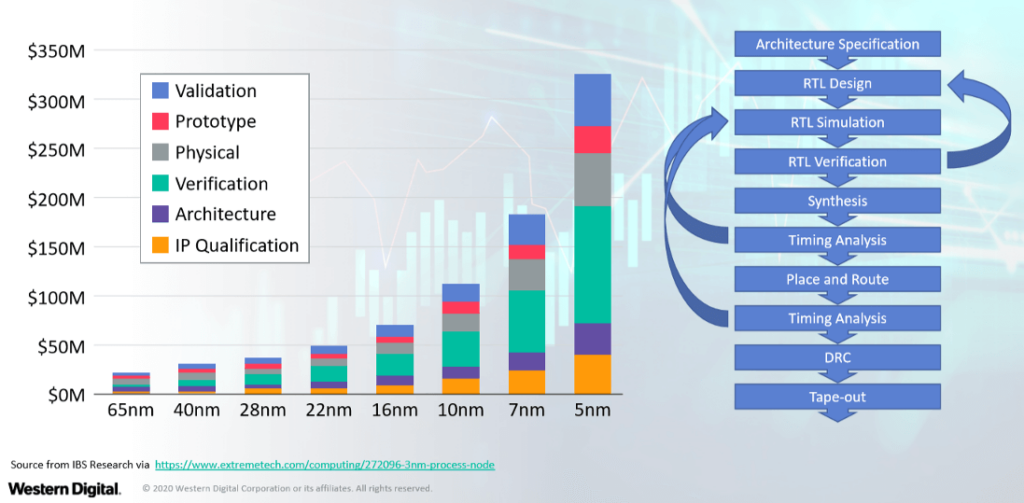

During the technology session, moderated by Jeffrey Wessel, VP Tosoh Quartz, Western Digital’s (WD) Richard New, VP of Research, touched a hot topic: open-source hardware. As a major supplier of mass storage devices, WD is in the center of today’s data explosion. While open-source software has enjoyed significant growth, open-source hardware has not found broad market acceptance yet. With increasing development cost (Figure 1) open-source hardware is looking more and more attractive.

WD, a member of the RISC-V Alliance and Chips Alliance, has shipped 1 billion 0pen source IP blocks. The open instruction set of RISC-V and the license-free access makes Risc-V attractive for a wide range of system designs. Because security is important, New pointed to Google’s activities in support of Open Titan.

Marco Pieters, VP, EUV product marketing, ASML, talked about planned improvements for extreme ultra-violet (EUV) lithography. ASML’s current stepper, NXE3400C, offers 170 wafers per hour (WPH) throughput. Customers are asking for more to make 3 nm and below economical. ASML is improving equipment uptime, resolution, alignment speed, numeric aperture, and WPH.

Chris Scanlan, VP WW Field Applications Engineering, JCET Group delivered the only IC package assembly presentation. JCET acquired STATS ChipPAC and is now the third-largest OSAT.

Scanlan said that edge nodes will capture, pre-process, and transmit vast amounts of data and contain many heterogeneous functions. He emphasized that JCET manufactures embedded wafer-level ball grid (eWLB) devices in volumes and is developing technologies like antenna arrays on substrate and antenna in package (AiP) for 5G.

Mobility

Oreste Donzella, EVP and CMO at KLA, introduced the Mobility session. He just returned from the Consumer Electronics Show (CES) 2020 in Las Vegas and conveyed how important semiconductors are becoming for electric vehicles (EVs) and internal combustion engine (ICE) powered vehicles.

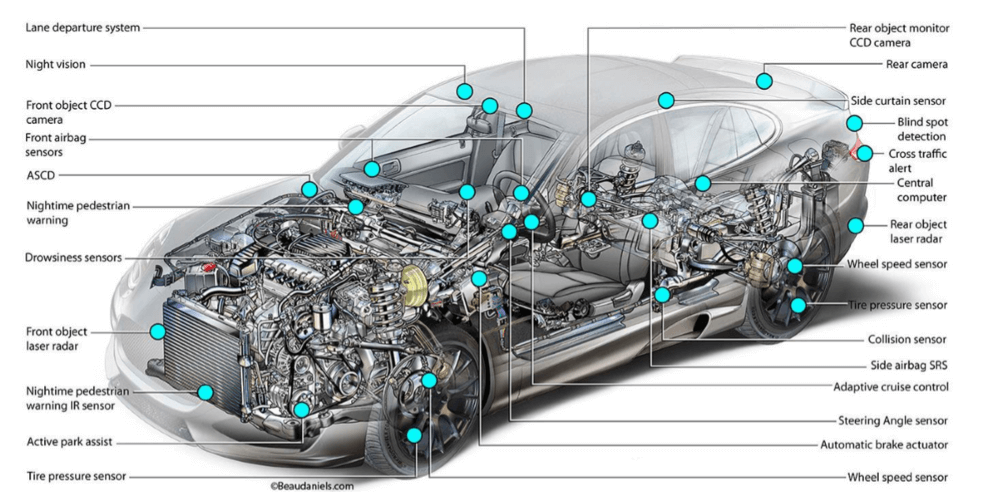

Ford’s CTO, Ken Washington said that Ford has had a Silicon Valley office since 2012, which now employs about 500 people. Semiconductors and software are playing increasingly important roles in new cars. Especially suppliers of MEMS and Sensors will like this slide (Figure 2).

Tim Frasier, President of Automotive Electronics, Bosch North America, explained how this privately held company, founded in 1886, reached $ $90 billion in revenue and became the largest automotive Tier 1 supplier. A 300 mm wafer fab in Dresden, Germany enables Bosch to also develop and manufacture consumer products and infrastructure for EVs, e.g. 450 kW chargers, that add 300 miles of range to an EV in 10 minutes.

Jody Kelman, Director, Self-Driving Platform at Lyft, passionately presented about the future of transportation. To substantiate the need for change, she conveyed these numbers:

- 80% of us drive to work alone; our car requires a parking spot there.

- On average we spend $ 700 monthly for this exclusive way of commuting.

- 96% of the time our cars are unused.

Kelman suggested we switch from thinking about transportation as an asset to transportation as a service, not only for cars but also for bikes, scooters – even rely on a smartphone with Lyft’s application to plan rides on public transportation.

5G

Rich Rice, Senior VP of Business Development at ASE US, introduced the speakers of the 5G session.

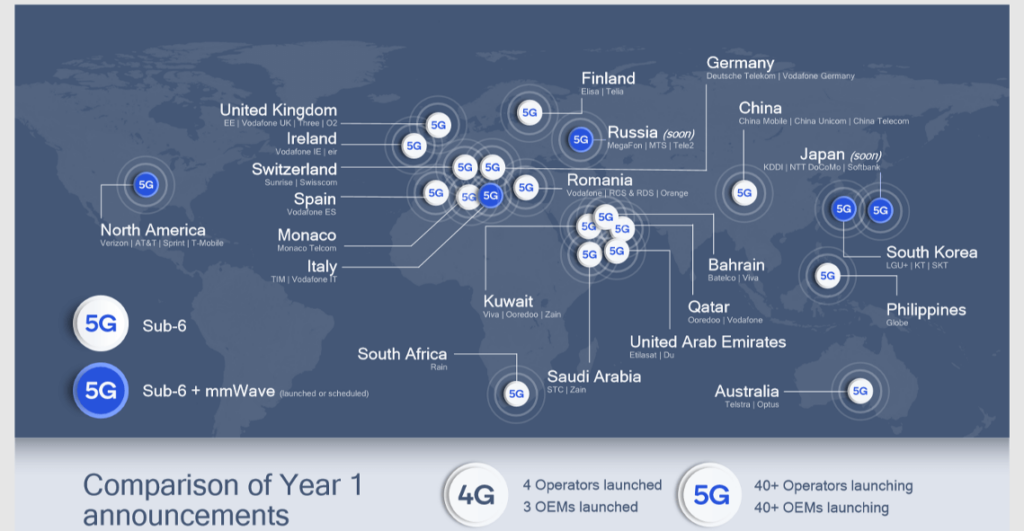

Qualcomm’s Gavin Horn, Senior Director Wireless Research, talked about 5G benefits and trade-offs versus 4G LTE. He showed which countries are planning to deploy 5G sub-6 GHz technology first, where governments and network operators are also deploying mm-wave technology right away and compared market acceptance of 5G with the 4G ramp-up. (Figure 3)

Horn also mentioned that 5G will significantly improve bandwidth and pointed out that handsets will need up to eight antennas to prevent users’ hands from blocking its signals. Another key point, mm-wave signaling requires line-of-sight!

Kevin Schoenrock, Director, Strategy & Planning at Qorvo (= RFMD + Triquint), emphasized that 5G handsets, as well as base-stations, will grow semiconductor revenues further. Schoenrock pointed out that 5G needs more filters than 4G, GaAs for power amplifiers as well as new IC packaging technologies and materials.

Mallik Tatipamula, CTO at Ericsson in Silicon Valley, focused on 5G infrastructure. He stated that network operators need to deploy many more base stations and change from the current central cloud concept to a distributed cloud network.

Asian Markets

Ben Rathsack, VP Tokyo Electron America, introduced the Asia Perspective session.

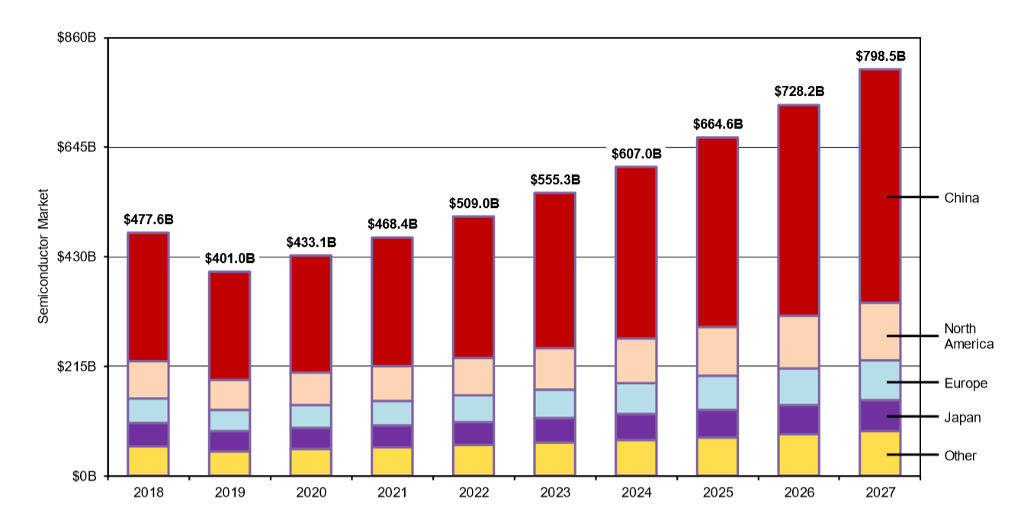

Handel Jones, CEO of International Business Strategies (IBS), confirmed that our industry suffered a 16% revenue decline in 2019, but projected growth for 2020 and beyond (Figure 4).

He said that while Chinese companies only supplied 3% of the semiconductors China needed in 2006, they supplied already 16% of an increased demand in 2019. He projected that China’s vendors will serve 40% of an even larger domestic market in 2030. Other points:

- China now has 700 million workers

- The average age of workers at HiSilicon is 33 years young

- Chinese PCs will not use the X86 architecture

- China makes big bets and large investments in semiconductors– the U.S. government doesn’t

Evan Rees, Analyst at Stratfor Asia Pacific, explained the conflict-rich history between Korea and Japan and showed South Korea’s 2:1 trade imbalance with Japan as well as Korea’s heavy reliance on Japanese chemicals for wafer processing. For example, the region relies on Japan almost 100% for photoresist. In exchange for Japan withholding chemicals, Korea’s demand for Japanese cars dropped 70% during 2019 – a small example of the lose-lose consequences of this trade war.

David Li, CEO of Cabot Microelectronics, lived in China for 15 years and observed China’s focus on 5G and AI. On a slide from Bloomberg, he showed that China’s total imports from the U.S. declined by about 30% in the last two years, while their semiconductor imports from the U.S. increased by more than 60%.

Simon Segars, CEO of ARM, outlined the company’s rapid growth and emphasized how important ARM’s 600+ alliance partners are. He stated that 3.5 Billion people use sophisticated smartphones today – many comprising ARM cores. 7.8 Billion cellular subscribers use 9.4 Billion cellular connections worldwide. Security is important in this big market. Segars mentioned that McKinsey values internet-of-things (IoT) related market (products and services) at $ 11 Trillion by 2035.

The Future of Moore’s Law

James O’Neil, VP, and CTO at Entegris, highlighted the many challenges the ongoing data explosion entails, then introduced the closing keynote.

Robert Chau, Intel Senior Fellow, Technology Development Director, Components Research, started with a bold statement: “The future of Moore’s Law is brighter than ever!” Then he showed that Intel considers their Embedded Interconnect Bridge (EMIB) and Foveros packaging technologies for side-by-side and vertical die stacking respectively, as natural extensions of Moore’s Law. He also called for new semiconductor materials, explained benefits of gate-all-around (GAA) transistors, praised EUV lithography and directed self-assembly (DSA) as key enablers for shrinking feature sizes.

How can an investor NOT own SemiCaps?

Last, but certainly not least, Clair McAdams, Managing Partner, Headgate Partners, moderated a panel discussion. It offered insights into Wall Street’s and investors’ thinking. The panel question: How can an investor NOT own SemiCaps?

Four industry veterans: Fred Lane, Paul Wick, Patrick Ho and Tom Rohrs addressed this question. The topics centered around the semiconductor equipment industry. Some key points: All panelists confirmed that this industry is becoming less cyclical and were optimistic about its future. memory vendors especially should do very well in the next few years. They confirmed that the equipment industry shrank from 7800 firms in 1990 to 3800 companies today and projected further consolidation in the subsystems and materials segment. They see AI as an important growth opportunity and pointed out that share repurchases in the U.S. are very high. Considering the U.S. – China trade conflict, they expect that China is still a good opportunity for equipment vendors, but only in the short term.

Conclusion and Personal Comments

Like in 2019, this year’s ISS presenters were very knowledgeable and covered a broad range of manufacturing topics. Also, the long breaks gave plenty of opportunities for networking and (I heard) the entertainment on Tuesday night was first class. However, the only presenter from the EDA / IP / Design community was Simon Segars from ARM. After:

- hearing from Lam’s Richard Gottscho about the high-value Conventor’s software adds

- hearing from Google’s Bradley Horowitz about Steve Jobs quote “It’s more fun to be a pirate than to join the Navy!”,

- reading Clayton Christianson’s book “The Innovator’s Dilemma”

- seeing advanced wafer fabs demonstrating how Big Data and AI improve throughput, yields and profits

- having my own experience with rolling out PrimeTime analysis software in a very unconventional way … and seeing that 20 years later PrimeTime still has 90% market share and is highly profitable

I haven’t given up hope that manufacturers will engage more with potential partners in EDA and IP to discuss how to leverage synergies between them.

The electronic (sub)systems our industry is planning, designing, and manufacturing are getting more complex and more difficult to manufacture cost-effectively. Advanced IC packaging, board, and system assembly and test companies can benefit significantly from closer cooperation. Yes, I understand, CapEx and ROI challenges limit the speed of change!

Thanks for reading this long blog…Herb