“Green shoots” refers to signs of economic recovery

As a former analyst, I always found forecasting for the next year in December to be the biggest challenge, and perhaps the biggest miss of the year. You essentially are working without a net. Historically calendar Q4 revenue estimates by the equipment companies are positive, as the semiconductor manufacturers are spending the last of their budgets. Capex budgets for the next year are typically not announced until the Q4 earnings announcements, and most PC and mobile phone forecasts follow the earnings announcements. Thus, there is less forward-looking information when you are forecasting in December than at other times of the year.

When SEMI ISS took place very early in January, I recall some years when the markets were changing so rapidly, presenters were adjusting forecasts up until the morning of the presentation. At the 2023 ISS, as posted in a January 2023 blog, analysts are predicting equipment to be down approximately 20% in 2023, and semiconductors revenues to decline in the 5% range; the bottom for equipment is estimated to be in Q3 o4 Q4 of 2023. There is a relatively good consensus on these numbers.

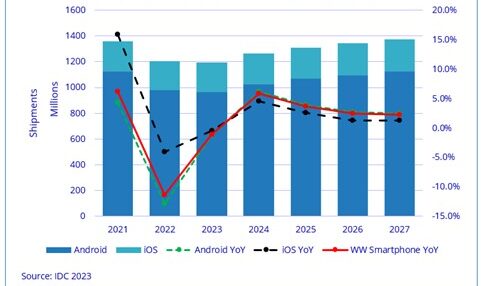

Now let’s move forward to the Q4 CY earnings reports that give a bit better insight into what may happen in 2023. To start with, Intel’s CEO Pat Gelsinger talked about green shoots appearing this past week. Several Wall Street analysts questioned the appearance of green shoots. From a PC and mobile phone perspective, there is little positive news. IDC announced on March 2 that they expect cell phones to decline 1.1% in 2023 with 5.9% growth in 2024. Most other industry earnings calls are still pretty negative on the market turning up any time soon.

Samsung, in its earnings call, was very cautious about discussing a turnaround, however, they were hopeful that sometime late in 2023 the rebound would begin. There is a lot of focus on leading-edge memory, which is where the most profitability lies. Samsung reported that PC makers are increasing memory capacity in the PCs. This is a pretty common method for PC makers to keep their pricing up while adding both lower-cost DRAM and NAND to their offerings hoping to entice customers to buy systems.

According to Nvidia’s report data center revenue is continuing to decline, as Nvidia data center revenues dropped 6% quarter over quarter. The earnings call attributed most of the decline due to a slowdown in China. Some consumer activities such as gaming and professional visualization had a rebound. Nvidia’s outlook was flat for the next quarter, so it is difficult to say if they are the lone bright light from a growth perspective as most other companies are forecasting flat to down revenues in Calendar Q1 2023.

Qualcomm had a 16% decline in revenue in the fourth quarter, semiconductors and handset revenue were both down 20% while automotive was essentially flat. Qualcomm is forecasting at best flat revenues for the first quarter of 2023.

Intel’s revenue was down 6% and PCs were down 18%. The outlook is fairly dim as Intel forecast a 20.6 to 26 percent decline in Q1 revenue.

In the Applied Materials earnings call they commented that the IoT, communications, auto, power, and sensing ICAPS, offset the decline in memory revenue. The forecasts from NXP and Infineon support these comments but NXP and Infineon are forecasting a flat Q1, but there have also been multiple announcements in the power semiconductor space regarding future expansion, which will bolster the 200mm market AMAT is forecasting a slight slowdown of approximately 4% in calendar year Q1 for 2023.

ASM had an interesting outlook a bit counter to the rest of the industry, as they reported a stronger first half of 2023, and expect a slower second half. Since ASM ALD and epi equipment are associated with leading edge, and SiC manufacturing which is based upon earnings calls will continue to see growth in 2023

If we look at what is happening at the foundries. Utilization is down at SMIC and UMC, running in the 90% range for Q4. TSMC announced that utilization is down as well but didn’t offer specifics. TSMC also announced that revenues will be down in the first half by potentially high single-digit numbers. TSMC also expects a second-half rebound, but not necessarily due to an overall upturn; although, in the Q&A there were some comments regarding how the peak in inventory occurred in Q3 of 2022. TSMC expects 3nm to be fully utilized early on which might be the growth driver for the second half of the year. TSMC also commented that automotive was still strong but according to TSMC the end of the shortage appears to be in sight. TSMC expects revenues to grow in 2023, albeit slightly.

What does 2023 Hold?

So, what does the future look like? As Yogi Berra is credited with saying, “It’s difficult to make predictions, especially about the future.

Lam Research reports that it expects the wafer fab equipment outlook to be in the mid-70 billion range for 2023, with 2022 being in the mid-90 billion. (Figure 2)

Figure 2:Quote excerpted from Lam Research December 2022 Earnings presentation.

ASM discussed a drop in wafer front-end (WFE) in the mid to high teens. ASM also commented on the resilience of advanced logic and automotive-related power/analog segments.

What the above numbers suggest is that WFE for 2022 will be up by low single-digit numbers, and 2023 will be down in the 20% range. Current predictions are that due to the number of fabs being built that WFE rebounds in 2024. The last two WFE downturns have been 1-year occurrences: however, history shows that most WFE downturns, especially those where there is a large inventory oversupply have been 2 years, which might suggest a low single-digit decline in 2024. While new fabs are being built history shows they don’t necessarily have to put equipment in place until there are signs of positive market conditions.

There are 2 wild cards that I think will have the largest impact on what the future holds. 1) China. At this moment there has been a limited impact on equipment sales. The biggest impact thus far has been AMAT’s sales to China which declined 10% year over year in their January earnings report. Other companies’ numbers are mostly negative year over year but less than 10% at the moment. The question here is if limits are placed on the trailing edge equipment sales, or if China decides to utilize national vendors where they can for trailing edge technologies. It’s also possible that the impact of the sanctions hasn’t shown up in earnings yet, and we will see that in the first quarter.

2) And what takes place in the industrial and automotive space. In the current economic environment, it appears companies are starting to look at how to conserve cash. This may mean that industrial plant expansions may slow for 2023, and resume later in 2024 as the economy improves. There is also the question of automotive if TSMC is correct and we are nearing the end of that shortage, will that also cause a slowing in production, especially if due to the economy new car sales begin to slow down?

As the pundits revise their forecasts in Q1 with greater visibility for the year it will be interesting to read the assumptions and see where their numbers lead the industry for the remainder of 2023 and into 2024. I’m currently betting on a slow 2 years for equipment, as both the electronics industry and the economy recovers from the whiplash of the past 3 years.