2020 was a roller coaster of a year from both a forecasting perspective and trying to keep up with shipments. At SEMI’s 2020 ISS in January, most pundits had a slightly positive outlook for the year. IHS was forecasting 5.5% growth. IC Insights was in a similar range forecasting 8% growth in January of 2020

Gartner was forecasting a second consecutive year of decline in CapEx, dropping 3.6% from 2019. Then COVID-19 hit the world in March. No one quite knew what to expect. Most pundits revised their forecasts down at the end of March and then again in May. Semiconductor and semiconductor equipment companies gave little guidance at the end of the March quarter. TSMC forecasted a flat year in their March quarter due to the uncertainty. To compound the situation the US department of commerce engaged in a trade war with China that looked like it could have a significant impact on both the semiconductor manufacturers, and semiconductor equipment manufacturers, and shipments of semiconductors were shut off to Huawei.

It was looking like doom and gloom for the industry. The hopes of a positive year for both semiconductors and semiconductor equipment seemed to evaporate. Dan Hutchinson in the VLSI December 2020 newsletter writes, “No forecast could have predicted this last December and neither did VLSI. The iIndustry went from a positive 5-8% growth rate to a flat to slightly negative growth rate in the April to May time frame.”

5G and Edge Computing to the Rescue

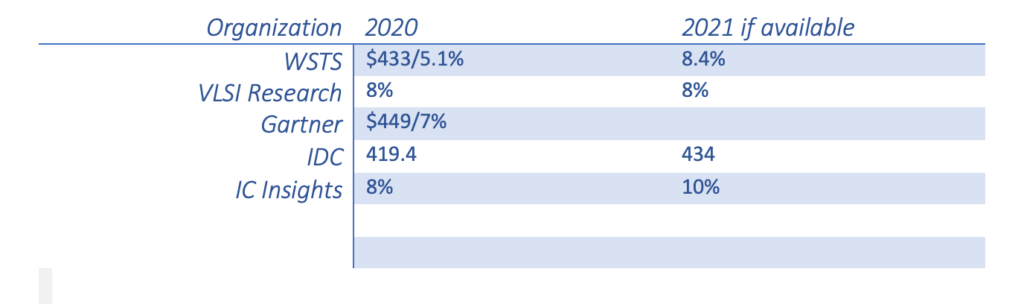

In June, the momentum was looking better, and then at the end of the September quarter it was fairly obvious that the year would end on a positive note for most semiconductor companies, as well as their semiconductor equipment counterparts. The year-end December and October forecasts by most analysts had increased their semiconductor forecasts to positive 5% or greater. The WSTS in their November report raised their forecast from 3.3% to 5.1%, Gartner in their December 2020 forecasts added another $17 billion to arrive at $449 billion in 2020 up from $419 billion in 2019 to predict 7% growth for the year. The year-end forecasts by select research groups are shown in Table 1.

It should also be noted that it was the year of the foundry, or more precisely the year of TSMC. 5G and high-performance computing, which likely includes artificial intelligence (AI) applications, helped TSMC grow revenues by 31% year-over-year by the end, according to their Q4 financial release this week. Intel, in spite of its supposed troubles, should end the year with positive growth of close to 3% if Q4 forecasts are accurate.

At the moment 5G, AI, and edge computing are expected to be key logic drivers. As the Q4 fiscal announcements roll out, we will have a better picture of the high-end logic space. In the trailing edge logic space, automotive is experiencing a shortage, so it looks like there will be broad growth in the logic space in 2021.

In the memory world, Micron in its Q1 21 fiscal year announcements, said it believes that DRAM is at the bottom of the cycle and that NAND supply will slightly outstrip the mid 20% demand that Micron is projecting. Expected growth in mobile phones, 5G infrastructure, and heterogeneous computing should help memory see some growth in 2021.

OSATS are also enjoyed strong growth. ASE, while not yet reporting Q4 revenues, has released their monthly revenues. The preliminary growth is at 15% year over year, and according to news reports in Digitimes and Taipei Times, packaging capacity is expected to be tight in 2021, driven by the same factors as the logic industry in 2021.

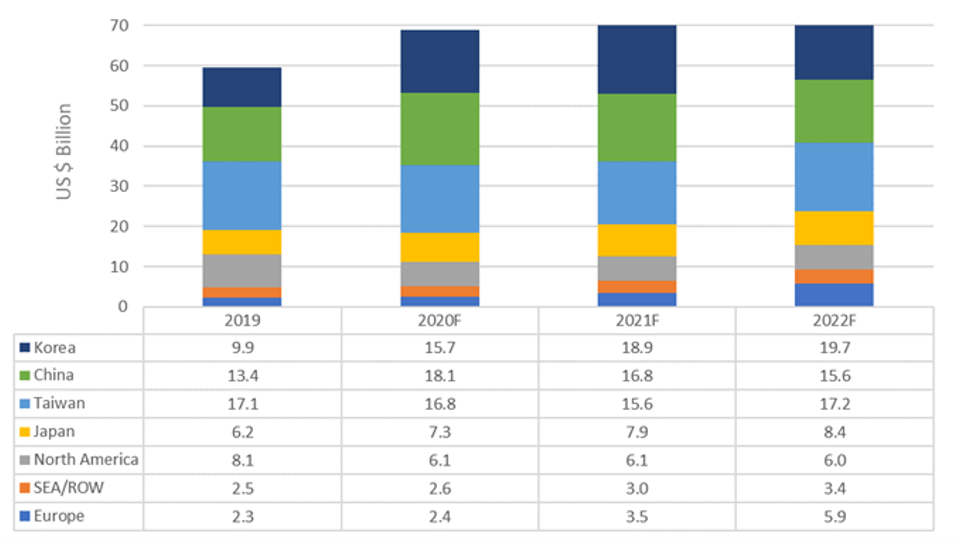

Semiconductor equipment companies also shared in the 2020 growth. According to SEMI, semiconductor equipment revenue is expected to increase from 59.6 billion in 2019 to $68.9 in 2020, reaching 16% growth year-over-year in an extremely robust year driven by 10nm, 7nm, and 5nm technology growth.

From a CapEx perspective, TSMC, Intel, and Samsung should account for nearly half of the industries CapEx, so it doesn’t appear that Intel will be shipping too much of their capacity to TSMC in the near future, but with a new CEO some of the decisions to outsource FPGA and GPU may change, but we will need to wait until Pat Gelsinger fully takes over to see what, if any, changes happen in 2021 at Intel.

Lam Research and Applied Materials showed h growth in both sales and service over 20% in the calendar year 2020, with ASML only estimated to grow revenues 13% year-over-year. So, a very nice year for the top three equipment companies, especially when at the end of the first quarter, things were extremely uncertain.

What does the Future Bring?

As 2020 demonstrated, forecasting is not for the faint of heart. SEMI’s ISS conference typically has multiple industry forecasters releasing their 2021 forecasts. This year with the virtual conference there were fewer presentations.

If one looks at the economic outlook, 2021 doesn’t look promising; however, neither did 2020 after March. According to Catherine Mann of Citibank, the economy is expected to see a rebound in 2021, but due to the contraction of 2020, the net gain will be slight.

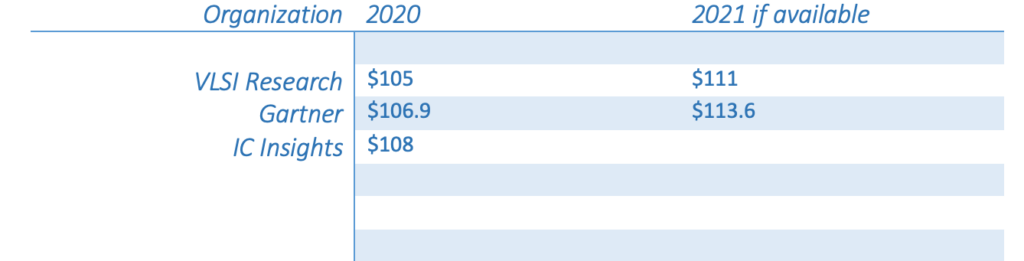

The chip and equipment forecasts presented above suggest a very robust 2021 from a chip perspective. From an equipment perspective, TSMC’s announcement last week of a $25 plus billion CapEx budget suggests it’s going to be a very good year for equipment companies; although, on the memory front Micron is looking at a flat CapEx, and some preliminary news out of Korea suggests that Samsung and Hynix will follow suit. This is likely what is leading to the approximately 5% increase forecasted by VLSI and Gartner for CapEx, and SEMI’s conservative equipment spending forecast; surprisingly, none of the forecasters have included TSMC’s CapEx surprise or some of the rumors that Samsung may try to keep pace in logic spending to stay competitive at 5nm and then 3nm. Intel supposedly will start to prep for 7nm production sometime in 2021, which means EUV investment at a price tag of approximately 150 million euros per tool. This leaves considerable upside for CapEx and the equipment segment in 2021, provided consumer and industry demand keeps up.

With the above information, 2021 looks to be a promising year for CapEx and chip companies, with the potential for upside. Time will tell if the pundits’ crystal balls have pointed them in the right direction for 2021.