2016 was a turning point for fan-out (FO) packaging. With Apple’s entrance and its subsequent decision to package its A10 APE in TSMC’s fan-out solution, the market changed. Thus advanced packaging leaders decided large investments for the development of fan-out platforms, impacting the related equipment and materials market. “Indeed, both equipment and materials markets for fan-out wafer level packaging (FOWLP) will reach an impressive 40% compound annual growth rate (CAGR)”, confirms Jérôme Azémar, Technology & Market Analyst, Advanced Packaging & Semiconductor Manufacturing at Yole Développement (Yole).

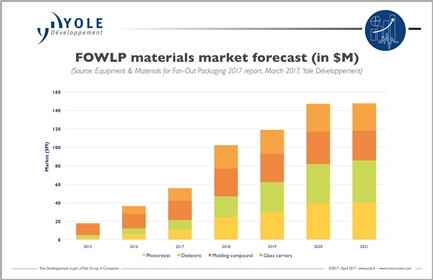

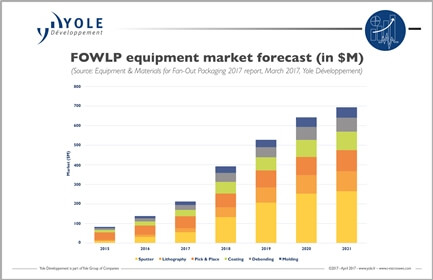

A detailed description of both markets and a list of equipment and materials studied by Yole is available in the new report Equipment and Materials for Fan-Out Packaging. According to this technology & market analysis, the total FOWLP equipment market is expected to reach about US$694 million in 2021 at an impressive CAGR of 42.5% between 2015 and 2021. Similarly, FOWLP’s total materials market is expected to reach about US$148 million in 2021 at a CAGR of 40% during the same period.

How is FO success driving the equipment & materials market? What is the impact of the huge investments listed during the 2015-2016 period? Under this dynamic context, where are the business opportunities? Yole’s advanced packaging team is expecting a lot of changes in the coming years and offers you today a snapshot of these industries.

In its report, the “More than Moore” market research and strategy consulting company proposes a clear picture of new investments and future markets for equipment and materials in Fan-Out. This report focuses on FOWLP’s key process steps, which Yole believes are the most essential to the platform: carrier bonding/debonding, chip placement, molding and redistribution layer (RDL) processing.

The equipment studied in the report that enables the aforementioned process steps includes pick-and-place bonders, lithography tools, sputter tools, molding tools, carrier debonding tools, and coaters/developers. In parallel, key materials investigated in Yole’s report include RDL dielectrics and photoresist, molding compound, and glass carriers.

As mentioned, 2015 – 2016 period saw large investments in FOWLP. “With the FOWLP adoption spreading from mobile/wireless and automotive to MEMS, RF SiP, and medical, a wealth of lucrative business opportunities exist for fan-out equipment and materials suppliers”, details Jérôme Azémar.

2017 will not see the same investment level, but the potential for new moves is high. Capacity enlargement is still an option for players considering it; in fact, it may be required in two years if fan-out keeps growing in high-density applications. Newcomers will gain some market share, necessitating entry into volume production. However, with 4.5 million wafers to be produced in 2021, capacity must also be increased by TSMC and/or other actors. Therefore, the second wave of investment must occur soon or capacity will not be sufficient to address the FOWLP market if it continues growing.

2017 will not see the same investment level, but the potential for new moves is high. Capacity enlargement is still an option for players considering it; in fact, it may be required in two years if fan-out keeps growing in high-density applications. Newcomers will gain some market share, necessitating entry into volume production. However, with 4.5 million wafers to be produced in 2021, capacity must also be increased by TSMC and/or other actors. Therefore, the second wave of investment must occur soon or capacity will not be sufficient to address the FOWLP market if it continues growing.

As a consequence, growth will be significant for all equipment and material types, indicating broad benefit from the FOWLP platform’s success. However, the challenges and market landscapes are very different from process step and the market is quite diversified. For example, lithography for patterning RDL represents one of the largest market components thanks to the equipment’s high value and the large volume of photoresist. In lithography, a “stepper”-type litho tool is used for FOWLP RDL patterning in order to achieve low-resolution (down to 2µm today), but its cost is high and manufacturers are under strong pressure to reduce their prices. “This market is currently dominated by Ultratech, which supplies TSMC, and Rudolph which has enjoyed success with OSATs”, says Santosh Kumar, Senior Technology & Market Research Analyst at Yole. And he adds: “We expect other players to penetrate this area, potentially with different approaches like laser ablation.”

As a consequence, growth will be significant for all equipment and material types, indicating broad benefit from the FOWLP platform’s success. However, the challenges and market landscapes are very different from process step and the market is quite diversified. For example, lithography for patterning RDL represents one of the largest market components thanks to the equipment’s high value and the large volume of photoresist. In lithography, a “stepper”-type litho tool is used for FOWLP RDL patterning in order to achieve low-resolution (down to 2µm today), but its cost is high and manufacturers are under strong pressure to reduce their prices. “This market is currently dominated by Ultratech, which supplies TSMC, and Rudolph which has enjoyed success with OSATs”, says Santosh Kumar, Senior Technology & Market Research Analyst at Yole. And he adds: “We expect other players to penetrate this area, potentially with different approaches like laser ablation.”

Other steps, i.e. mold compound processing, may be more prone to domination by a single player. This symbolic step, which creates a reconstituted wafer out of a mold in which the IC are encapsulated, is almost entirely owned by Nagase Chemtex, almost 90% market share on the materials side. Nagase Chemtex’s dominance is the result of the complex approach such chemicals require in order to develop an optimum solution, and the long history Nagase has with the main producers including Nanium and STATS ChipPAC. liquid molding compound (LMC) is currently the preferred FOWLP mold material, however, to break Nagase’s monopoly and reduce cost, other materials suppliers are working to develop granular-type molding (GMC) materials. By 2021, GMC is expected to have 29% of the total market. On the equipment side, things are more diversified, with APIC, Yamada, and Towa the key compression molding tool suppliers for FOWLP.

A detailed description of Equipment and Materials for Fan-Out Packaging 2017 report is available on i-micronews.com, advanced packaging reports section.

Source: http://www.yole.fr