Takeaways from the SEMI Capex and Capacity Seminar

With Nvidia announcing its earnings in May, it brings closure to the CY Q1 financial calendar. Because of geopolitical and economic uncertainty, the earnings calls had slightly different outlooks over the timing of the quarterly financial announcements, from Micron in April to Marvel in late May.

To help its members understand where the semiconductor and semiconductor equipment market is heading, SEMI held a Capex and Capacity Seminar focused on architecting growth in the AI era. Hosted by Joe Stockunas, it featured Ajit Manocha, President & CEO, SEMI; Dr. Handel Jones, Founder and CEO of IBS; and Clark Tseng, Sr. Director, Market Intelligence SEMI presenting.

Ajit kicked off the conversation, giving a high-level overview of the market. How AI helps semiconductors, and how semiconductors help AI. AI has driven the semiconductor market for the last 2 years, and SEMI believes it will be the key driver accounting for 50% of the growth of the chip market through 2030, when, at that time, quantum computing will possibly be ready to become a key driver.

Dr. Handel Jones then covered the semiconductor market in detail and gave great insight to Ajit Manocha’s introduction. Jones broke his talk down into three segments.

- An analysis of the semiconductor industry.

- An analysis of the foundry market.

- The impact on Capex

He then gave concluding remarks.

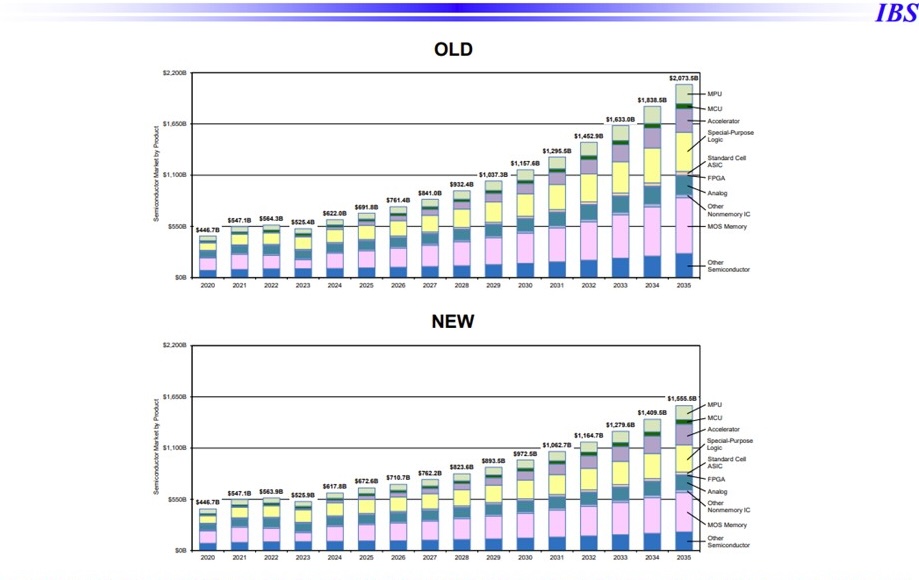

Jones started with an updated forecast of the semiconductor market. He concluded that, due to tariffs, there would be a decline in revenue from previous forecasts. The semiconductor market will reach $972 billion in 2030, just shy of the $1 trillion mark. However, by 2035, semiconductor revenue will be valued at $1.55 trillion, growing from a forecasted $672 billion in 2025. Jones expects that technology less than 2nm will be the biggest driver of CapEx and semiconductor revenue.

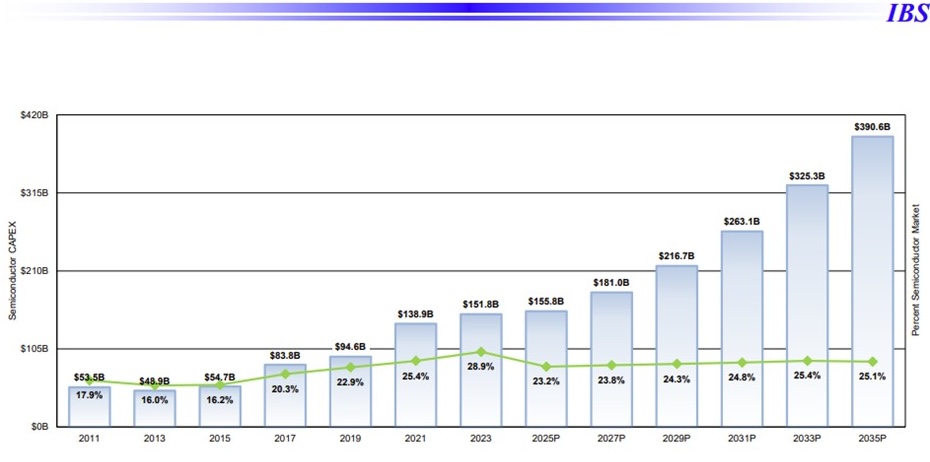

Growing from an estimated 240,000 wafer starts per month(WSPM) in 2030 to 590,000 WSPM in 2035, Jones estimates it will take $194 billion in Capex to meet the 2030 capacity levels, roughly $38 billion a year over the next 5 years.

About one and a half fabs would be built each year to support 2nm. The capex will be focused primarily on advanced logic, advanced memory, and advanced packaging to support 2.5 and 3D packages.

The revised IBS semiconductor forecast has 2025 pegged at $672 billion, with 2026 and 2027 forecast at $710 billion and $762 billion, respectively. The key drivers are expected to be high-performance computing (HPC) and AI chips. Processors and accelerators will account for the logic component, and high bandwidth memory (HBM) for driving memory.

IBS is forecasting slow growth for the consumer, automotive, and wireless markets. One bright spot in the legacy semiconductor market could be in the power semiconductor segment. Power management devices are critical for EV automotive, the power grid, and data centers. With the strong growth in those segments, power management chips could see stronger than market-average growth.

Figure 2: According to the Semiconductor Revenue Forecast, a reduction in growth of the semiconductor market is due to the impact of tariffs. (Source: SEMI Capex and Capacity Seminar May 2025.)

IBS commented that the foundries will be the biggest drivers of 2nm, including TSMC and Samsung, And now that Intel has embraced a foundry model even for its own chip designs, foundries will be the largest source of semiconductor revenue and procurement of equipment in the semiconductor marketplace.

IBS expects the ratio of Capex to semiconductor revenue will continue to rise. One would expect this to be true due to an increase in process complexity, increasing lithography costs due to Hi-NA EUV, or an increase in multiple patterning. However, the ratio declines from 28% in 2023 and reaches 25.1% in 2035. So it rises above 2019 values but does not beat the 2023 peak.

Dr. Jones concluded by commenting that the current tariff situation will have a near-term growth impact, but that WFE looks to be strong over the next 10 years.

Clark Tseng of SEMI then presented on SEMI’s outlook for the year.

The worldwide tensions are slowing GDP growth, with all regions forecasted to see a decline. The USA is now expected to grow only 1.8%, and China is expected to grow at 4%. This will have an impact on the purchase of electronic goods and, as a result, semiconductor sales. While semiconductor sales are strong year-over-year, quarter-over-quarter is slowing, and in some cases, negative for Q1 and the forecasted Q2. Fab utilization is running below 70% and is expected to rebound in Q2 of 2025 as electronic goods manufacturers gear up for back-to-school and holiday sales.

Some of the positive vibes are thought to be a result of companies pulling in imports to possibly beat any tariffs that might be forthcoming. SEMI reiterated that AI and cloud computing are the key drivers, with 40% of semiconductor equipment going to build chips that support HPC applications.

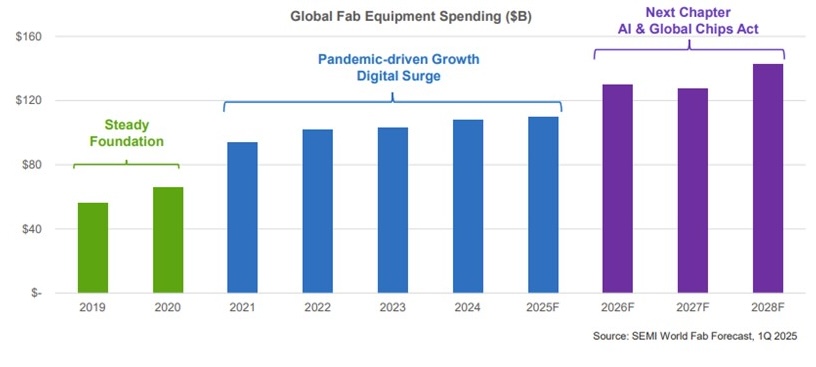

Tseng then discussed the fab investment trends that started in 2019. He described it in three phases, the steady foundation, followed by pandemic spending, and then the next growth period driven by AI and the global chips acts, where regions are looking at semiconductors as being strategically important so there is a need for both new capacity and technology to support this agenda.

Each region is investing massive amounts of capital. Semi projects in 2028, the Americas will spend $33 billion in Capex, a $9 billion increase. SEA is spending $7 billion, Europe $15 billion, Japan $18 billion, China $28B, and Taiwan $30 billion. China is the only country with a spending decline from 2024, having spent $63 billion in 2024 to support its internal chip industry. By 2028, SEMI expects Logic to increase capacity by 8.7%, Memory by 2.6%, Discrete by 5.2%, and Analog by 5.8%.

Tseng concluded with some similar points that were heard from IBS.

- Near term, the results are impacted by the uncertainty of the trade market and tariffs.

- AI will be the key driver of semiconductor revenue and capital expenditures.

- Regional investments will drive diversity in the semiconductor market, impacting the supply chain.

My key takeaways from the presentations suggest that if you are closely involved with HPC, your market will be strong over the next 5-10 years. Foundries will be the key drivers of technology and the purchasing of process equipment. Supply chains will need to adjust to accommodate the re-regionalization of the semiconductor market. And the industry is looking at steady growth over the next 10 years as the AI boom carries us along.